A cash balance plan layered on top of your 401(k) unlocks significantly higher tax-advantaged savings for business owners and key employees, without abandoning the flexibility your rank‑and‑file team relies on. At 401GO, we handle the complexity behind the scenes so you get control, clarity, and powerful savings. Start with a custom projection to see exactly how much more you can contribute, and whether a combo plan fits your business goals.

Cash Balance Solutions

Why Cash Balance Matters

A Cash Balance Plan Adds Real Value

- A cash balance plan promises a pay credit plus an interest credit to a hypothetical account. The employer, not the participant, bears investment risk.

- For owners and executives in high-earning years, cash Balance plans allow contributions well above 401(k) limits (given proper design).

- Use it in tandem with your existing 401(k) or profit-sharing plan to retain benefits for all employees.

- Helps create more efficient tax deductions in high-income years while still maintaining competitive benefits.

Cash Balance Solutions

Who Should Consider It

Is a Cash Balance Plan Right for You?

- Business owners, professionals, or leadership-heavy firms seeking larger tax-advantaged contributions

- Companies with stable cash flow and forecastable earnings

- Firms already using or planning to continue a 401(k) for broader employee population

- Must comply with nondiscrimination, coverage, and actuarial rules under defined benefit law

How Cash Balance Works

The Mechanics in Plain Terms

Pay Credit

Each year, the employer applies a defined formula (e.g. a percentage of compensation) to participants’ hypothetical accounts.

Interest Account

That hypothetical balance accrues a guaranteed interest credit, often tied to a fixed rate or index.

Hypothetical Account

Participants see an annual balance, but it’s not their choice to invest; employer bears the risk.

Distribution of Benefits

At plan termination or participant separation, benefits may be distributed as a lump sum or an annuity, per plan terms (rollover eligible in many cases).

Additional Details

Because it’s a defined benefit plan under ERISA, annual actuarial valuations, funding, and testing are required.

Cash Balance Solutions

Dual Plan Strategy: Cash Balance + 401(k)

Why Combine with Your 401(k)?

- A combo strategy allows you to maintain 401(k) benefits (deferrals, match, catch-up) for employees while layering aggressive contributions for owners.

- It can help with nondiscrimination and coverage testing when structured appropriately.

- Participants keep access to deferrals, in-plan Roth, and other familiar features.

- Flexibility in design: e.g., Safe Harbor match, discretionary profit-sharing, custom allocations.

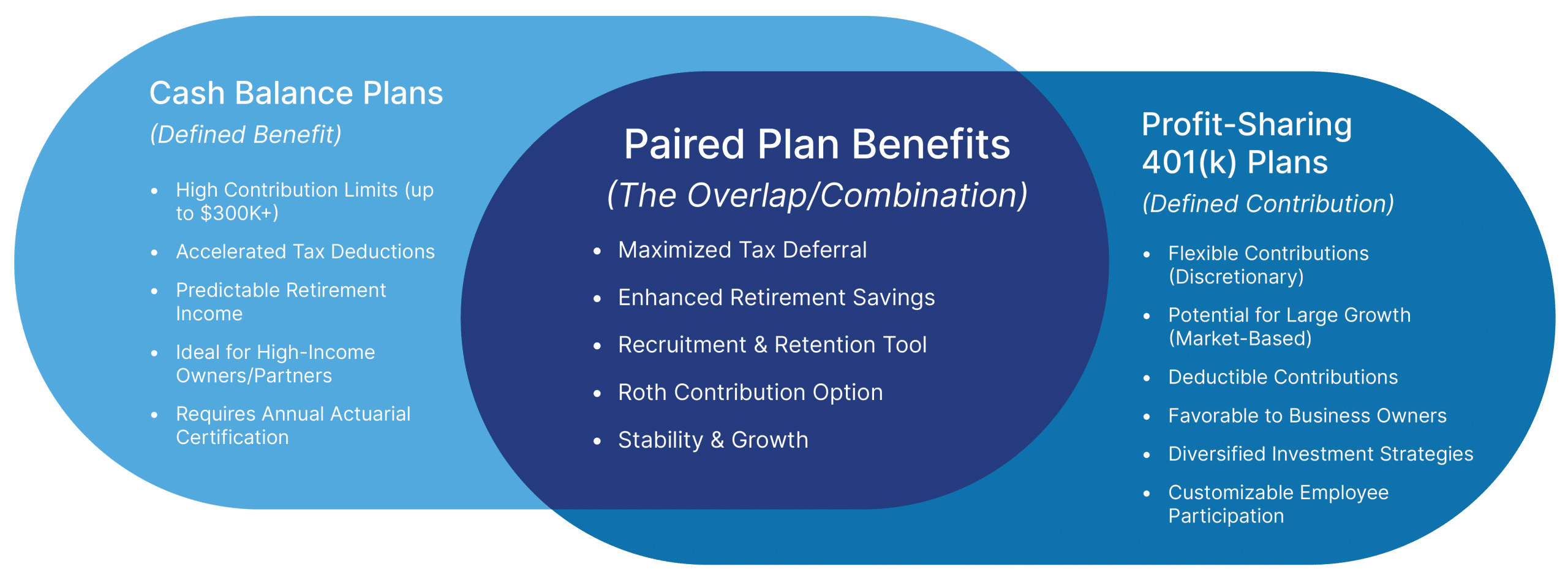

Retirement Plan Comparison

Cash Balance vs. Profit Sharing 401(k)

Cash Balance Plans (Defined Benefit)

These plans are primarily designed to allow owners to make very large, tax-deductible contributions to rapidly build retirement savings. They function much like a traditional pension plan.

- High Contribution Limits (up to $300k+): Contribution amounts are calculated based on the retirement benefit goal, often allowing for much higher annual contributions than a 401(k) alone.

- Accelerated Tax Deductions: The large contributions are immediately tax-deductible for the business, significantly reducing current taxable income.

- Predicitable Retirement Income: The plan targets a specific benefit at retirement, providing a set rate of return (e.g., 4% or 5%) to participants, regardless of market performance.

- Ideal for High-Income Owners/Partners: The large contributions are highly effective for owners looking to “catch up” on retirement savings or lower a substantial tax burden.

- Requires Annual Actuarial Certification: Contributions are mandatory and calculated precisely by an actuary each year.

Profit Sharing 401(k) Plans (Defined Contribution)

This is a flexible, market-based plan that forms the foundation of most modern retirement programs, benefiting both owners and employees.

- Flexible Contributions (Discretionary): The employer can choose the amount of the profit-sharing contribution each year (including zero), providing flexibility during lean years.

- Potential for Large Growth (Market-Based): Participant accounts grow based on investment performance and market returns.

- Deductible Contributions: Employer matching and profit-sharing contributions are tax-deductible for the business.

- Favorable to Business Owners: Owners can participate in matching contributions and receive a disproportionately large share of the profit-sharing contribution (through “cross-testing” or “new comparability” formulas).

- Diversified Investment Strategies: Participants can choose from various investment options, offering control over risk and potential growth.

- Customizable Employee Participation: Employees can contribute via salary deferral (pre-tax or Roth) and receive employer contributions.

Paired Plan Benefits (The Overlap/Combination)

When combined, these two plans work in tandem to offer the maximum legal tax shelter and a competitive benefits package.

- Maximized Tax Deferral: This is the chief benefit. The business can deduct the massive cash balance contribution plus the profit-sharing/matching contributions, leading to the highest possible annual tax deduction for the company.

- Enhanced Retirement Savings: Allows business owners to contribute and defer tax on over $500,000 annually in some cases.

- Recruitment & Retention Tool: Offering both a 401(k) (flexibility) and a defined benefit plan (security) creates a highly attractive and robust retirement package for employees.

- Roth Contribution Option (401k Side): The 401(k) portion allows for Roth employee contributions, providing tax-free income in retirement, which is not available in the Cash Balance plan.

- Stability + Growth: The Cash Balance plan provides a floor of stable, guaranteed returns, while the 401(k) offers market-based upside potential.

Cash Balance Solutions

Cost, Administrative Burden & Mitigation

Managing Complexity Without Surprises

- Cash Balance plans require actuarial expertise, annual valuations, compliance reports, and funding discipline.

- With 401GO’s tech-enabled admin, much of that complexity can be managed with minimal burden on you.

- Transparent pricing structures help minimize surprises; fixed tiers or per-employee fees keep cost expectations clear.

- Audit support and compliance review are included in your plan’s service offering.

$3500 Annual Fee

0.3% AUM Fee

Client Testimonials

See What Our Clients Say

”By layering a cash balance plan, we boosted our deductible retirement savings by six figures, while keeping our existing 401(k) for our team.

”401GO’s team handled all actuarial work and compliance behind the scenes. Our CFO sleeps easier.

Frequently Asked Questions

FAQs About Cash Balance Plans

What is a cash balance retirement plan?

A defined benefit plan that credits pay credits and interest credits to hypothetical accounts.

How complex is administration?

Complexity exists: valuations, funding, testing, but 401GO’s stack handles most of it for you.

Can I combine a cash balance with my 401(k)?

Yes. You can maintain your 401(k) for employees while layering a cash balance for high savers.

Who is eligible to sponsor a cash balance plan?

Broadly, any employer eligible to offer qualified retirement plans must design its plan to pass IRS/ERISA rules.

When must the plan be established/funded?

Typically, by your business tax return due date (including extensions), and funding on an annual schedule.

Let’s Get Started

Ready to Explore Cash Balance?

- Request your custom cash balance estimate

- Schedule a call with a plan specialist

- Download our detailed combo plan whitepaper