Saving for retirement is one of the most important—and often overwhelming—financial goals. For those using a 401(k) to build their nest egg, the Internal Revenue Service (IRS) sets annual contribution limits to help you maximize your savings while adhering to federal guidelines. Each year, these limits are adjusted, typically as a response to inflation and other economic factors.

For 2025, there’s some great news: contribution limits are increasing once again. Here’s what you need to know about the new limits, how they can help you save more, and what this means for businesses sponsoring 401(k) plans.

The New 2025 Contribution Limits

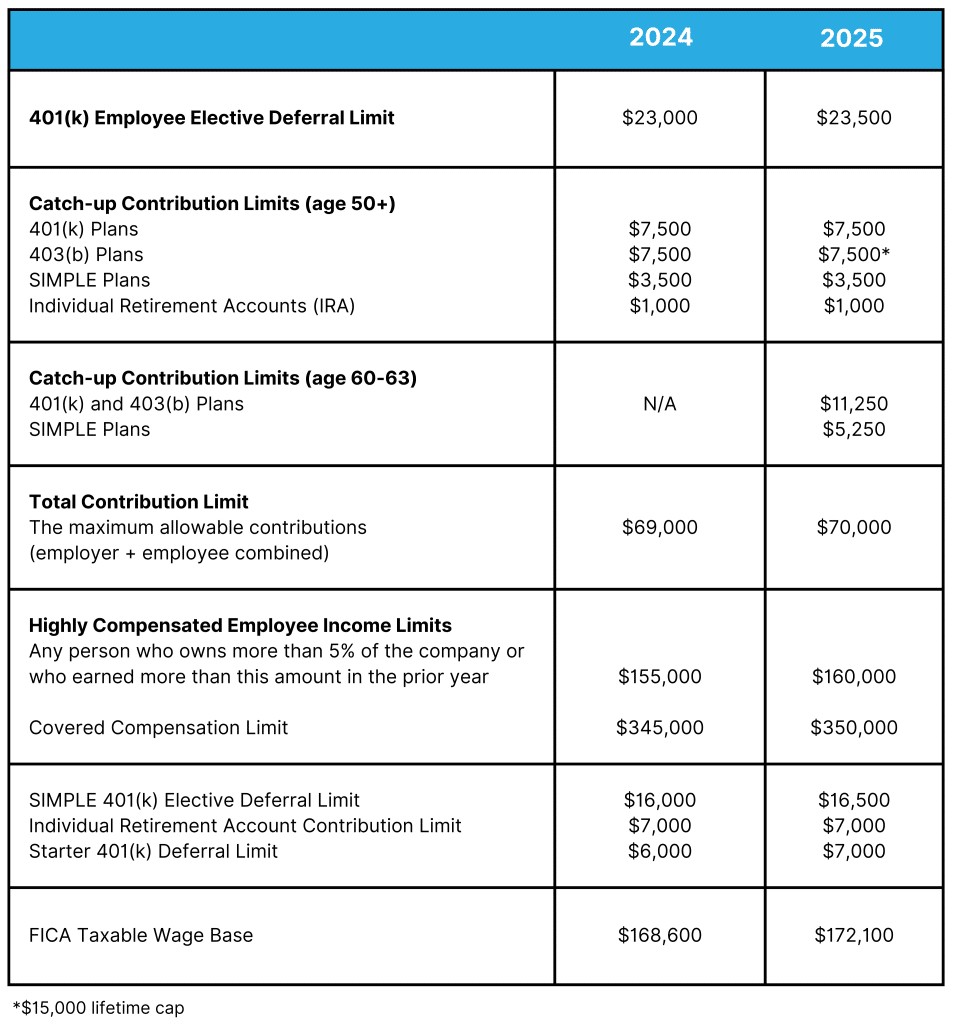

For 2025, the IRS has increased the annual 401(k) contribution limit to $23,500, an increase of $500 from 2024. This applies to employees who participate in traditional 401(k), 403(b), most 457 plans, or the federal government’s Thrift Savings Plan.

Workers aged 50 and older are still allowed to make additional “catch-up” contributions. This catch-up limit remains at $7,500 for most plans in 2025, allowing those nearing retirement to contribute up to $31,000 annually for most 401(k), 403(b), governmental 457 plans and the federal government’s Thrift Savings Plan. A new feature in 2025, SECURE Act 2.0 added additional catch-up contributions for employees aged 60-63, in the amount of $11,250.

Beyond employee deferrals, the combined limit for all contributions (employer match + employee contribution) is now set at $70,000, an increase from $66,000 in 2024. For employees aged 50 and over, this combined limit goes up even further to $77,500 if you include catch-up contributions.

How to Maximize Your Savings

If your employer offers a match, make sure you’re contributing enough to take full advantage of it. For example, if your company matches 50% up to 6% of your salary and you’re earning $100K, setting aside 6% ($6,000) means you’ll receive an additional $3,000 in matching contributions. That’s $3,000 added to your account each year. Employees who don’t contribute to their full match are leaving money on the table.

While it would be ideal, we know that contributing the maximum amount immediately isn’t feasible for everyone. If you can’t max out your 401(k), try increasing your contributions incrementally. For example, increase your contribution rate by 1% of your salary each year or after every raise.

If you’re 50 or older, use the catch-up contribution option to supercharge your retirement savings. The additional $7,500 can make a substantial difference, particularly if you got a late start on saving.

Remember to automate your contributions so you can save consistently without thinking. This is an easy way to ensure you’re steadily working toward your retirement goals.

How These Changes Impact Businesses

For businesses sponsoring 401(k) plans, the new limits bring both opportunities and challenges.

First, if your business offers a matching program, higher employee contributions could increase costs. However, offering a competitive 401(k) match is a powerful tool for attracting and retaining top talent, especially in today’s tight labor market. For smaller businesses, even modest matching programs can make a big difference in employee satisfaction and loyalty.

Businesses need to pay close attention to the IRS rules for highly compensated employees (HCEs), which include individuals earning more than $160,000 in 2024 or owning more than 5% of the company. Ensuring your 401(k) plan remains compliant and nondiscriminatory is crucial. Consider adopting a Safe Harbor 401(k) plan, such as those offered by 401GO, which simplify compliance and eliminate certain nondiscrimination testing in exchange for agreed-upon matching or contribution requirements.

For small to mid-size businesses, budgeting for increased contributions is essential. Changes like employee raises, new hires, or higher participation rates could lead to higher matching costs. However, these higher matching costs could result in more tax deductions for your company. Proactively planning for these potential expenses will help your business stay financially prepared while maintaining a valuable benefit for your team.

Build a Stronger Future for Your Workforce

The increase in 401(k) contribution limits for 2025 is an opportunity for employees to save more and for businesses to demonstrate their commitment to employee well-being.

Offering a robust retirement plan helps businesses compete for top talent, boost morale, and foster long-term loyalty. If you’re looking for an easy and cost-effective way to implement or upgrade your 401(k) program, 401GO is here to help.

With 401GO, you can easily set up a compliant, affordable 401(k) plan tailored to your business needs. Our technology streamlines plan management so that you can focus on growing your business while supporting your employees in building a secure retirement. Get started with 401GO today!