With more and more states passing retirement mandate legislation, the retirement planning landscape is about to change dramatically. Millions of employees will have new options to save for retirement, and small businesses will be under a lot of pressure to demonstrate they’re in compliance with the new mandates. There’s a big knowledge base that needs to be built out by professionals who know what they’re doing, and financial advisors will play a vital role in guiding small-business owners through the complex business not only of implementing these new mandates, but also of avoiding incurring penalties for non-compliance.

The Genesis of State Mandates

There’s no doubt that Americans should be saving more for retirement. According to a 2019 survey, half of American households have no retirement savings at all, including almost half of all Baby Boomers, a generation that’s either already reached, or is quickly approaching retirement age.

In an effort to address this crisis – and prevent future generations from meeting the same fate – many states have instituted mandatory retirement saving programs for small businesses. While each state’s legislation is unique, these programs generally mandate that businesses that don’t already give their employees a way to save for retirement offer them an employer-sponsored retirement plan or a state-run retirement program.

While we agree with the general idea behind these plans – more people should definitely save for retirement – the mandatory, one-size-fits-all government approach leaves a lot to be desired for small-business owners who like to stay lean, mobile and efficient. Here at 401GO, that’s our whole business model; helping small-business owners set up the best retirement plans available without all the hassle that goes with traditional investment bank plans. Still, state mandates are a good start.

Understanding State Retirement Mandates

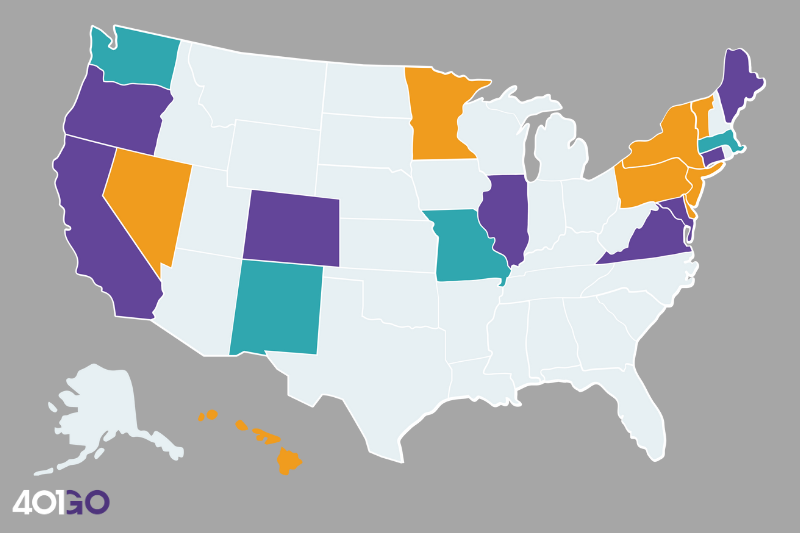

So far, 18 states have passed state retirement legislation. California, Colorado, Connecticut, Illinois, Maryland, Massachusetts, Oregon, and Virginia have passed the laws and actively implemented the programs. New Jersey has passed legislation and scheduled implementation. And Delaware, Hawaii, Minnesota, Nevada, and New York have passed the laws but haven’t yet scheduled implementation. In addition, several other states are considering passing similar legislation.

These state-mandated retirement programs are intended to address the fact that only half of businesses with 100 or fewer employees offer retirement plans, and only 4 in 10 small business employees with incomes in the bottom quartile have the option of retirement savings through their employer. Employers in these states that don’t already offer retirement plans must offer either a private retirement savings program, or enroll their employees in a state-sponsored retirement program. These state-sponsored retirement plans are generally Roth IRAs; with this type of retirement account, employee contributions are deducted from their post-tax income, so their eventual retirement withdrawals will be untaxed. (This is in contrast to a traditional IRA, which is generally funded with pre-tax income, and which is subject to taxes upon withdrawal.)

Enrolled employees will contribute around 3% to 5% of their post-tax wages to their retirement fund. These state-mandated programs often require employers to automatically enroll employees, and use investment firms that are selected by state agencies – which is one of the programs’ biggest drawbacks. While government is great at rolling out large-scale programs, they generally don’t have the expertise to maximize the investments they handle. This is a great opportunity for savvy financial advisors to intercede; employees can opt out of contributions, and place that money elsewhere.

There’s an opportunity with employers, too. Most states require employers to perform significant administration for these retirement plans, which is a specific area where financial advisors can offer valuable counsel. Steering small-business owners to use private retirement services like 401GO can pay big dividends; while these services often come with small fees, they offer a streamlined, simplified service. While the state retirement programs are free, they come with a lot of paperwork; in most states, there’s very little payroll integration, and deductions have to be done manually each month. Most busy small-business owners will gladly use a paid service if it frees up valuable bandwidth.

The Importance of Compliance

Finally, keep in mind that each state retirement program is unique, and comes with different deadlines, eligibility requirements and employer exemptions. Compliance and education is a big opportunity here. Financial advisors who want to advise businesses on this issue will have to stay current on the particulars of each program. In a rapidly evolving field like this, it’s best to stick to authoritative sources of information like state government websites, reputable industry publications and fellow financial professionals.

While the exact standards vary from state to state, employer compliance is going to depend on two main factors: the number of employees they have, and how long the company’s been in operation. If the employer meets those standards, they then have to prove that they offer a payroll-deducted retirement savings plan for their employees, whether it’s a private account or through the state program. Each state also has a unique timeline for implantation; for example, Illinois is requiring all small businesses to come into full compliance by November 2023, while Maine is giving small businesses until April 2024.

Penalties for non-compliance can be steep. In Illinois, employers who don’t comply with the state mandate face fines of $250 per employee for the first year, and $500 per employee in year two. In Oregon, non-compliant employers could face fines of up to $5,000 per calendar year.

Retirement Mandates: Stay Tuned

Big picture: State retirement mandates are probably a net gain. They’ll get more people saving for retirement, including a lot of people who’ve never had the opportunity to save for retirement through their job. Still, they’re best viewed as a starting point. Many employers are going to opt to offer their employees private retirement plans, and they’ll need help implementing these programs, and managing the massive administrative burden that goes along with them. They’ll also need advice on choosing the appropriate plans for their diverse workforce, and how to maximize participation rates. Above all, they’ll need help managing costs.

There’s a massive opportunity here for motivated financial advisors who specialize in outreach and education, who can proactively help employers handle the requirements of these new mandates.