Several states require that employers meeting certain standards offer their employees retirement savings benefits. Here, you can learn which states these mandates apply to.

Let our experts show you how 401GO offers a far superior alternative to state-provided options.

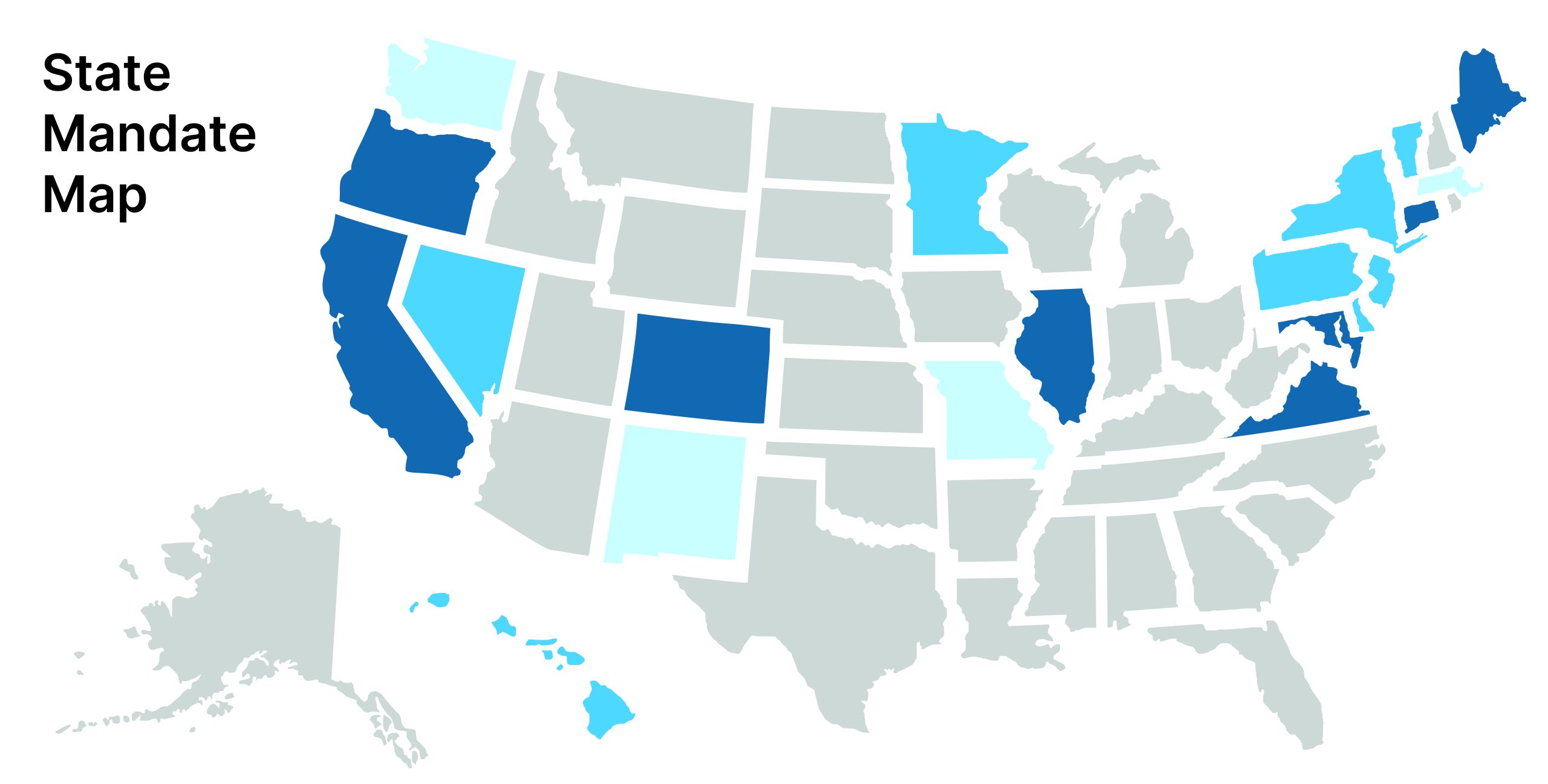

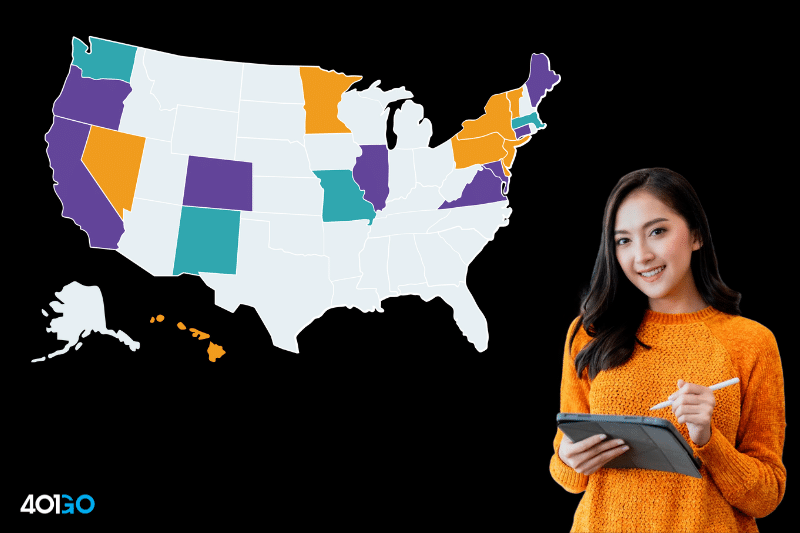

State Mandates

Learn Your Alternatives

Although the details vary from state to state, most are requiring businesses with 5 employees or more to offer a retirement benefit to their employees.

Businesses can choose to use the state-managed program, which is usually a payroll-deduction Roth IRA, or purchase a qualifying alternative privately. Either way, a decision must be made that affects employees.

About half of affected businesses are choosing a private option, and among those that use the state plans, many later change their minds.

The retirement landscape has changed drastically for small businesses, and most can afford a much better benefit than they imagined. Take a look at the details for your state and compare it to the 401GO alternative.

California

Active plan, all deadlines passed. Penalties apply.

Colorado

Active plan, all deadlines have passed. Penalties apply.

Connecticut

Active plan, add deadlines have passed. Penalties apply.

Delaware

Active plan. All deadlines passed. Penalties apply.

Hawaii

Legislation passed. Implementation TBD.

Illinois

Active plan. Penalties apply.

Maine

Active plan. All deadlines passed. Penalties apply.

Maryland

Active plan. Deadline is December 31, every year.

Massachusetts

Active, voluntary MEP for non-profits only.

Minnesota

Active plan. Deadlines: Soft launch and voluntary enrollment for any size covered employer Jan. 19, 2026 to March 30, 2026, 100 or more April 1, 2026 to June 30, 2026, 50 to 99 July 1, 2026 to Dec. 31, 2026, 25 to 49 Jan. 1, 2027 to June 30, 2027, 10 to 24 July 1, 2027 to Dec. 31, 2027, 5 to 9 Jan. 1, 2028 to June 30, 2028. Penalties apply.

Missouri

Not operational yet.

Nevada

Active plan, all deadlines passed.

New Jersey

Active plan, all deadlines passed. Penalties apply.

New Mexico

Inactive.

New York

Active plan. Deadlines: Employers with 10 or more employess that have been in business for at least 2 years. March 18, 2026, if they have 30 or more employees. May 15, 2026, if they have 15 to 29 employees. July 15, 2026, if they have 10 to 14 employees

Oregon

Active plan, all deadlines passed. Penalties apply.

Pennsylvania

Pending legislation.

Rhode Island

Active plan. Deadlines: Businesses employing more than 100 eligible employees must comply no later than October 15, 2026; Businesses employing between 50 and 99 eligible employees must comply no later than October 15, 2027; and Businesses employing between 5 and 49 eligible employees must comply no later than October 15, 2028. Penalties apply.

Vermont

Active plan, all deadlines passed. Penalties apply.

Virginia

Active plan, all deadlines passed. Penalties apply.

Washington

Currently offering a voluntary marketplace; will institue mandates like other states. Legislation signed, with a program to launch January 2027.

State Mandates

Download the free guide to secure choice retirement plans.

With secure choice plans being offered in more and more states, it’s important for businesses to understand enough details to make an informed decision. Retirement plan decisions can have far-reaching consequences for both employer and employee.

State mandated retirement plans are typically Roth IRAs, which have different rules and regulations than 401(k) plans.

Plan designs and mandates vary from state to state, but most have some basic similarities that will help you make a smart choice.

This guide will help you know what to consider when choosing a retirement benefit.

Client Testimonials

See What Our Clients Say

Frequently Asked Questions

Questions? We’ve Got Answers

Is it legally required in all U.S. states for employers to provide retirement plans to employees?

In most states, employers are not required to offer retirement plans. However, a few states do have these requirements, and several more are working on legislation. See the list above for details.

What counts as an employer retirement plan?

While 401(k)s are the most common employer-sponsored retirement plan, other options include SIMPLE IRA plans, SEP plans, profit-sharing plans, cash-balance plans, and stock ownership plans. Each state has rules about what types of plans will count as an exemption from the state plan, so it’s best to consult your state regulations.

Do employees like the state plans?

Obviously, opinions vary. A payroll-deduction IRA is more powerful than a private IRA, and both of those are better than no retirement option at all. However, many bad reviews of the state plans can be found, and most of them focus on communication and education issues and poor support.

By contrast, 401GO has a 4.8-star rating and leads the industry for customer support.

Do employees have to participate in state plans?

Most states offer auto-enrollment IRA plans, meaning employees will be automatically added to the plan, and contributions will be taken from their paychecks. However, employees are always able to opt out of the plan, and stop and start contributions anytime.

Many 401(k) plans also have auto-enrollment features, always with the ability to opt out, so education and communication with employees is important.

What are the penalties for not offing a retirement plan?

These penalties vary from state to state. Those states that have mandates in place will almost always have penalties attached for those who don’t comply. It’s best to consult your state to determine the exact penalties and deadlines.

News and Blog Articles

See Our Recent Blog Posts

Filter

Let’s Get Started

Start Your Journey with 401GO

401GO offers 401(k) retirement savings plans that are far superior to state mandate options. How much better? Find out for yourself by beginning the plan setup process right now.