States are celebrating their secure choice retirement mandates as a major solution to the American retirement crisis, but workers say otherwise. In fact, 70% say they don’t want to save in a government-run IRA, and more than a third go as far as to opt out of the plan.

Do workers know something that legislators don’t? Or do lawmakers have selective vision when making rules that govern enormous pots of money?

Consider these very obvious problems.

Limited Choices

Some will say that a few choices are better than no choices at all, but that’s certainly open for debate. For example, in some states the default investment is intended to earn nothing. It aims to earn zero, and to lose zero. But participants pay for the privilege of putting their money in this non-interest earning fund. They would be better off stuffing their cash in the mattress.

Even with those investments that earn money, the dividends are usually small. An investor with a small amount of education and ambition could easily get a better return from a private IRA, a brokerage account, or sometimes even a money market account at their local bank.

Limited Portability

Portability was touted as a feature of state secure choice plans, but it doesn’t take much looking to discover that portability of these accounts is a bigger problem than a solution. The idea of the account belonging to the participant instead of to the employer is solid, but the practicalities get in the way.

The portability only works if the participant moves from one secure-choice-participating employer to another. And since most states have fewer than half of their businesses participating, the likelihood of multiple jobs all offering the same plan is low. What happens to the state-run IRA account if the employee moves to a company with a 401(k)? What if the participant pursues employment in another state?

Now the employee is saddled with an account that no longer functions as intended (as a payroll-deduction plan) and cannot be rolled into a 401(k). Participants are left to pay for an account they may no longer be using, or withdraw the funds and pay taxes on them. Most of these funds never make their way into another retirement account. Is this good for workers?

Limited Flexibility

Most of the states are implementing Roth IRA plans, which are good for some, but certainly not for all. Since they are designed to cater to a broad population, they are not suitable for everyone’s financial circumstances or goals, and they do not come with the ability to select a non-Roth option.

Roth accounts tend to be useful for younger workers, who will probably have a larger income in retirement than they do currently. They are often less useful for older workers who are at the peak of their earning potential.

Roth IRAs do not allow employer contributions, so even those businesses that can afford it and want to contribute cannot do so with this type of plan. Add to that the much, much lower contribution limits of an IRA as compared to a 401(k), and you have two big reasons why the earning potential within a 401(k) is far greater than with an IRA.

And the flexibility problems don’t end there. High-income earners are often not eligible to contribute to an IRA. And those employees who have private IRAs already will not increase their savings potential at all, since contribution limits are not enforced per account, but rather per person. In fact, employees that aren’t watching closely could find themselves in trouble if they over-contribute because they now have two separate IRA accounts.

Government Involvement

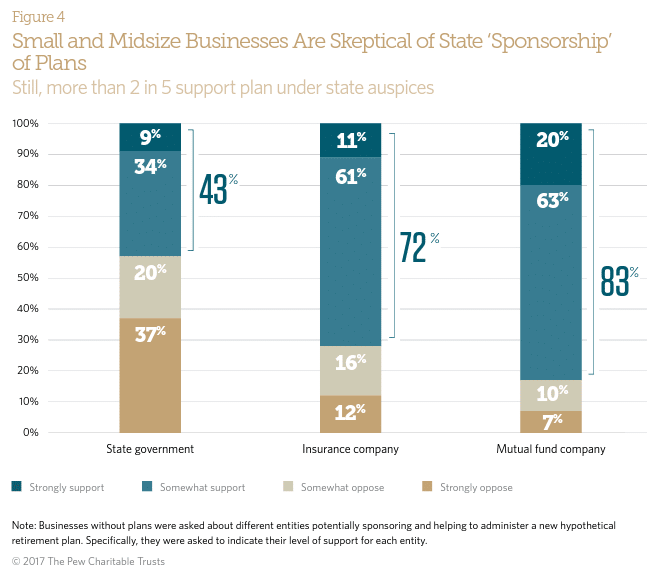

Secure choice plans are all created by state legislation, and all overseen by government entities. Governments, even those in the most responsible states, are not known for their competence or efficiency, leading most small business owners to prefer that states engage a private company to provide the management. Do you really want the government involved in your retirement savings? Trust in government sits at an astoundingly low 14%.

The upside of government involvement (at least theoretically) is worker protections, but since state IRA plans are not subject to ERISA rules, those protections do not apply.

And consider the potential for political interference, turning retirement accounts into political weapons. Or changes to legislation that might make it difficult for workers to plan appropriately. Or restrictions to participants’ freedom to use their funds. And what happens if the federal government makes laws that interfere with the state laws?

Who really has the power over these plans?

Fees, Fees, Fees

Because state IRA plans are free to employers, it is the workers who pay all the fees. In some states these fees are within industry norms (at least for now), but in others the fees are very high. California, for example, charges almost a full 1% to participants, triple what they would pay with a privately-held IRA.

These fees add up over time, not just in dollar amounts, but also in lost growth. The fees paid to managing bodies are dollars that could have been earning much-needed dividends. And, if they are invested in funds that are not bringing a good rate of return, the fees could actually make them lose money in their retirement savings accounts.

Which leads me to wonder, who benefits from state IRA plans?

The Players that Benefit Most from Secure Choice Retirement

It’s hard not to see state-mandated retirement plans as a money making scheme for the government and a very small number of private companies. Just two big corporations manage almost all of the state plans. States are creating new regulatory and oversight boards, and vast bureaucracies to manage accounts and serve participants.

Increasingly, the movement looks like one big “good ol’ boys” club, aimed at enriching the wealthy and empowering the powerful at the expense of the average American employee.

It’s not as if the retirement industry was pure as the wind-driven snow before the states stepped in. The legacy retirement plan providers are behemoth companies that have spent their energy focusing on whales — the largest businesses with the wealthiest retirement plans. For four decades, they have ignored the vast majority of workers, those that work for small companies.

It’s no accident that the state solutions started coming about at the same time that fintech solutions were entering the market. The need was so great that someone had to act. But in terms of which has the power to make a substantial difference for workers, fintech 401(k) plans are vastly superior to state IRAs.

For the sake of brevity, I’ll just mention a few quick bullet points to illustrate my point.

- Contribution limits for 401(k) plans are almost 10x what’s allowed in IRAs, making them a much more effective savings vehicle.

- Employers have the option to provide funds to their employees within a 401(k), again increasing their ability to save.

- Most of the fees are paid by the employer, so the fees to the participant are kept within reasonable limits. Because fintech companies are relying heavily on automation, they are able to keep costs very low for both employers and employees.

- While 401(k) portability is not as good as it could be, it is possible to roll one 401(k) into another, or leave the old one in place for what is often a reduced fee.

- Scrappy fintechs provide much better customer service than government bureaucracies. Governments have no competition and don’t care if you leave them a bad review.

- Fintech 401(k)s are built specifically for the market that is the most left behind and the most in need — small companies with fewer than 100 employees. In fact, even those with fewer than 5 employees can still get an affordable retirement benefit for their employees.

- New 401(k)s come with lots of tax credits. IRAs come with zero.

Don’t Fall for the Hype

If your company is one that is being forced to offer a retirement benefit, let me offer two pieces of advice.

First, at least investigate a fintech 401(k) option before choosing the state plan. There is a reason why more than half of small companies will choose a private option over a state IRA, and another 25% of those that choose the state plan will change their mind.

Second, seriously consider seeking the counsel of a good financial advisor. Regulations and economic forces of all kinds are plaguing small companies, and a smart advisor could save your company thousands of dollars, as well as helping setup and manage a good retirement plan.

Stick it to the good ol’ boys club and talk to 401GO. We can help you get a good retirement plan setup in just minutes at a price point you can actually afford.