In the ERISA landscape, “fiduciary” is more than a buzzword; it is a legal standard that carries significant weight. For advisors and plan sponsors, the 3(38) Investment Manager serves as a critical tool for risk mitigation and operational efficiency.

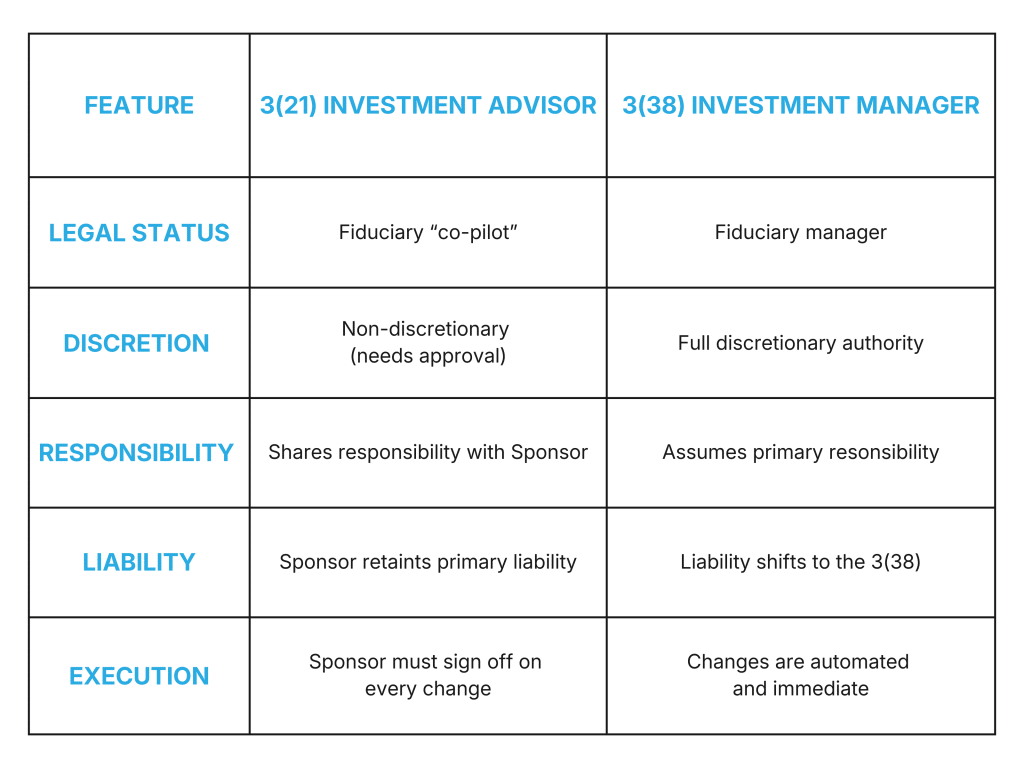

By definition, a 3(38) fiduciary is an investment manager who assumes full discretionary authority over a retirement plan’s assets. This is different from a 3(21) advisor who acts as a consultant, providing recommendations that the plan sponsor must ultimately approve. A 3(38) has the authority to execute investment decisions independently.

While a 3(21) advisor must wait for a signed approval from a busy business owner to swap a lagging fund, a 3(38) has the authority to act immediately on the plan’s behalf.

3(21) vs. 3(38): At a Glance

For an advisor, the choice between these two roles often comes down to how much liability they (or their clients) want to carry.

The Four Pillars of 3(38) Management

Acting as a 3(38) advisor isn’t just about selecting funds; it’s about maintaining a defensible fiduciary process. This involves four primary pillars:

- Selection & Diversification: Curating a menu that satisfies the “broad range” requirement of ERISA 404(c).

- Continuous Quantitative Analysis: Monitoring performance, expense ratios, and style drift against the plan’s Investment Policy Statement (IPS).

- Autonomous Rebalancing: Executing fund replacements immediately when a manager fails to meet established criteria.

- Fiduciary Audit Trail: Maintaining the documentation required to demonstrate procedural prudence during a DOL audit.

Integrated 3(38) Services at 401GO

We designed 401GO to function as the operational engine for your practice. Through our 3(38) services, we provide a structured investment solution that allows advisors to outsource the technical execution of the investment lineup.

By utilizing our 3(38) services, you can solve three pain points at once:

- ERISA 404(c) Safe Harbor: We provide a diversified array of investment options and the necessary disclosures. This can shield the plan sponsor from liability for losses resulting from participant-directed investments.

- Conflict Mitigation: Our models prioritize low-cost, institutional-grade funds. This ensures the lineup is optimized for performance rather than revenue sharing, aligning with the highest fiduciary standards.

- Scaling the Advisory Practice: Outsourcing the “power of the pen” removes the bottleneck of manual fund changes. This allows your firm to scale its 401(k) book of business without a proportional increase in administrative overhead.

The 3(38) investment lineup is reviewed and adjusted quarterly, ensuring the plan’s investment strategy remains healthy and compliant. This provides your clients with a premium investment experience while you focus on what you do best: providing holistic advice and building relationships.