Maxing out your 401(k) is a great start, but for high-income earners, it can often feel like trying to fill a swimming pool with a garden hose. Even with the total 401(k) limit rising, many business owners are still left with a massive tax bill and a savings gap.

Enter the cash balance plan. When paired with your 401(k), this hybrid strategy doesn’t just increase your retirement bucket; it replaces the hose with a fire hydrant. A cash balance plan and 401(k) combo allows high-income earners who are already maxing out their 401(k) to exceed standard contribution limits, often resulting in over $200,000 in annual tax-deductible contributions.

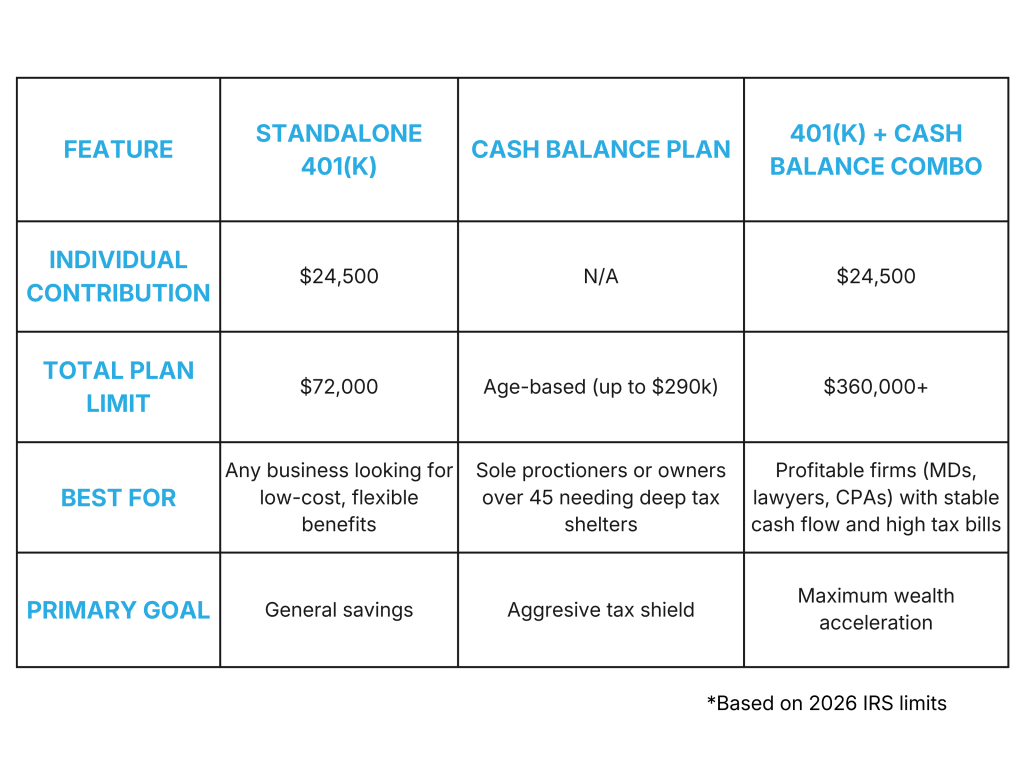

What is a cash balance plan?

Think of a cash balance plan as a pension in 401(k) clothing. While legally classified as a defined benefit plan, it looks and feels like a modern individual account to your employees.

In a traditional pension, the benefit is promised as a monthly check for life starting at retirement. In contrast, a cash balance plan defines the benefit as a hypothetical account balance. Each year, the employer adds two specific credits to this account: a pay credit (typically a percentage of wages or a fixed dollar amount) and an interest credit (a guaranteed rate, such as a fixed 4% or a variable market-linked rate). While the plan’s investment performance fluctuates, the employer’s obligation to the employee remains fixed based on these credits.

The important distinction between cash balance plans and a 401(k) plan is that the employer, not the employee, bears the investment risk. If the market underperforms, the company must ensure the guaranteed balance is met. Conversely, if the plan’s investments outperform the interest credit, the excess gains stay in the plan, allowing the company to reduce its future contribution costs.

One of the most valuable traits of a cash balance plan is the absence of the rigid contribution limits found in 401(k). Because cash balance plans are designed to hit a specific target balance by an employee’s retirement, the annual contribution limits are flexible, factoring in an employee’s age, income, and the time remaining until retirement. Additionally, while traditional pensions often calculate benefits based only on an employee’s final high-earning years, a cash balance plan builds a portable balance based on every year of service with the company.

Why a 401(k) + cash balance plan combo works

Combining a cash balance and profit-sharing 401(k) plan is a favorite strategy for high-income earners and professional service firms (like doctors or lawyers) for a few reasons:

- Tax Deductions: While 401(k)s have set annual limits, cash balance contribution limits are age-dependent. The older you are, the more the business can invest into the plan, sometimes exceeding $200,000+ annually. These contributions are tax-deductible for the business.

- Recruiting Power: In a tight labor market, offering a pension-style benefit alongside a 401(k) makes your compensation package stand out. It’s a unique benefit that retains top-tier talent.

- PBGC Protection: Most cash balance plans are insured by the Pension Benefit Guaranty Corporation (PBGC). This adds a layer of security that the standard 401(k) plan doesn’t have.

- Design Flexibility: You don’t have to give everyone the same slice of the pie. These plans can be cross-tested, allowing employers to provide different contribution levels for different groups of employees.

Is a cash balance plan right for your business?

Before you dive in, there are two things you need to know. First, cash balance plans require consistent cash flow. Unlike a 401(k) profit-sharing contribution, cash balance contributions are generally mandatory. You want to be sure your revenue is stable before committing. This is especially important if you’re a small professional firm (under 26 people). If this is the case, you likely won’t have PBGC insurance. This means you must be prepared to fund the plan.

Second, cash balance plans can be complex to manage. Historically, the administrative costs and actuarial requirements kept small businesses away.

At 401GO, we believe high-level retirement strategies shouldn’t be reserved for the ultra-wealthy. Our technology-first approach strips away the complexity and high overhead of traditional providers, making combining your 401(k) with a cash balance plan approachable, affordable, and easy to manage.