Saving for retirement just got a little more room to grow. The IRS announced new 401(k) contribution limits for 2026. If you’re a saver, business owner, or advisor helping clients plan ahead, these changes matter. Whether you’re maxing out your contributions or just getting started, understanding the new limits helps you make the most of your retirement plan.

The Numbers for 2026

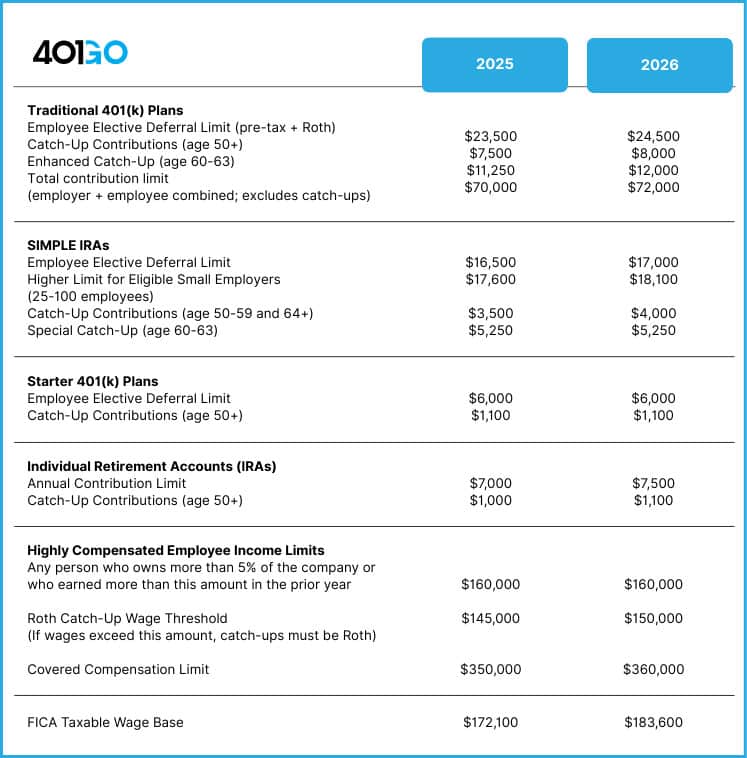

For 2026, the IRS raised the standard 401(k) contribution limit to $24,500, up from $23,500 in 2025. That’s the baseline for most employees participating in retirement plans.

If you’re 50 or older, you can contribute an additional $8,000 in catch-up contributions, bringing your total to $32,500. The SECURE 2.0 Act of 2022 includes an enhanced catch-up provision for participants ages 60-63. These individuals can contribute an additional $11,250 beyond the regular limit, for a total of $35,750.

Solo 401(k) plans follow the same employee contribution limits, but business owners get an added advantage. You can also make employer contributions on top of your employee deferrals, which can push total contributions up to $72,000 (or $80,00 with catch-up contributions for those 50 and older). These increases give employees and business owners alike more flexibility to build their retirement savings.

What’s New with Roth Catch-Up Contributions

Starting in 2026, if you make over $150,000 and you’re eligible for catch-up contributions, those extra dollars must go into a Roth 401(k) account instead of a traditional pre-tax account. This means you’ll pay taxes on those contributions now, but your withdrawals in retirement will be tax-free. It’s a shift that requires some planning, especially if you’ve been used to the immediate tax benefit of traditional contributions. If this applies to you, it might be worth reviewing your overall tax strategy with a financial professional.

Making the Most of the Higher Limits

How do you take advantage of these increased limits? Start by reviewing your current contribution rate. If you’ve been contributing a flat dollar amount or percentage, consider bumping it up to capture the new ceiling. Even small increases add up over time. If your employer offers a match, make sure you’re contributing enough to get the full benefit.

That’s essentially free money for your retirement.

For small business owners offering a 401(k) plan, communicating these changes to your team can help them adjust their savings strategy. Employees often don’t realize they can increase contributions mid-year, so a simple reminder can make a real difference.

What Businesses Need to Plan For

If you’re a business owner or work with a 401(k) plan provider, these changes come with a few action items. Payroll systems need to be updated to reflect the new limits, and employees should be notified of the increase so they can adjust their contributions if they wish. For companies evaluating 401(k) plans for the first time, 2026 is a great year to get started. With higher contribution limits, the value proposition for employees grows, and offering competitive retirement plans can help attract and retain talent. Plus, businesses may qualify for tax credits when setting up a new plan, which makes the investment even more worthwhile.

Moving Forward

The 2026 contribution limits open up new opportunities for savers and employers alike. Whether you’re looking to max out your own contributions, help your team save more, or explore retirement plans for your business, staying informed is the first step.

Have questions? Contact us today to learn more about contributions and the retirement plans we offer.